Medicare is one of the most important healthcare decisions you’ll make, but it’s also one of the most confusing. If you’re turning 65 or transitioning from employer coverage, understanding the system can feel like learning a foreign language. You’ll encounter an alphabet of Parts A, B, C, and D, along with enrollment timelines, late penalties, and more fine print than a mortgage disclosure. The good news is that you don’t have to figure it out alone.

In this blog, we’ll answer some of the most common Medicare from “Do I need both Part A and B?” to “What’s the difference between Medicare Advantage and Medigap?” Think of it as your starting place a way to get your footing before diving deeper into coverage comparisons.

Medicare: The Basics

Medicare is a federal health insurance program for people 65+ and for younger people with certain disabilities. It’s broken into “parts,” each covering different things.

Part A (Hospital Insurance): Covers inpatient care, hospital stays, hospice, skilled nursing facility care, and some home health services.

Part B (Medical Insurance): Covers doctor visits, outpatient care, preventive services, durable medical equipment, etc. There’s a monthly premium, deductible, and coinsurance.

Part D (Prescription Drug Coverage): Helps with drug costs. Plans vary. If you delay enrollment without creditable coverage, you may face penalties.

Medicare Advantage (Part C):Private plans approved by Medicare that bundle A, B, often D, and sometimes extras (vision, dental, etc.) into one plan. You have to use certain providers or networks.

Medigap (Supplemental Insurance): Add‑on plans to Original Medicare (A+B) that help cover copays, coinsurance, deductibles. Not compatible with Medicare Advantage.

Medicare FAQs

1. When Should I Enroll in Medicare?

You get a 7‑month Initial Enrollment Period (IEP): starts 3 months before your 65th birthday, includes your birth month, and ends 3 months after.

If you’re still working and have employer‑based coverage, there are Special Enrollment Periods that may allow delay without penalty.

If you miss the IEP and aren’t eligible for a Special Enrollment Period, you’ll have to wait for the General Enrollment Period (Jan 1 – March 31), and coverage starts July 1.

2. Do I Need Both Part A and Part B?

Part A is often premium‑free if you or your spouse paid enough Medicare taxes while working.

Part B has a monthly premium even if you don’t use services. If you keep employer insurance, sometimes you can delay enrolling in Part B to avoid paying two premiums. But that has to be handled correctly so you don’t incur a penalty.

3. How Much Does Medicare Cost?

Here are some of the 2025 figures from CMS / Medicare.gov to guide your budgeting:

Part A premium: Many people pay $0/month if they qualify because of work history. If not, it may cost either $285 or $518/month, depending on how long you or your spouse paid Medicare taxes.

Part A deductible: $1,676 per benefit period for inpatient hospital coverage.

Part B premium: Standard is $185/month in 2025. Income‑related adjustments may apply if your income is above certain thresholds.

Part B deductible: $257 in 2025. After that, you typically pay 20% coinsurance for most services.

Cost of Part D and supplemental coverage (Medigap) varies widely by plan, location, drug list, etc. Always compare plans in your ZIP code.

4. What Happens If I Miss My Enrollment Period?

Late Part B enrollment penalty = 10% increase in premium for every 12‑month period you were eligible but didn’t enroll. That penalty lasts as long as you have Part B.

Late Part D penalty applies too if you go 63+ days without creditable drug coverage. It’s added to your monthly premium.

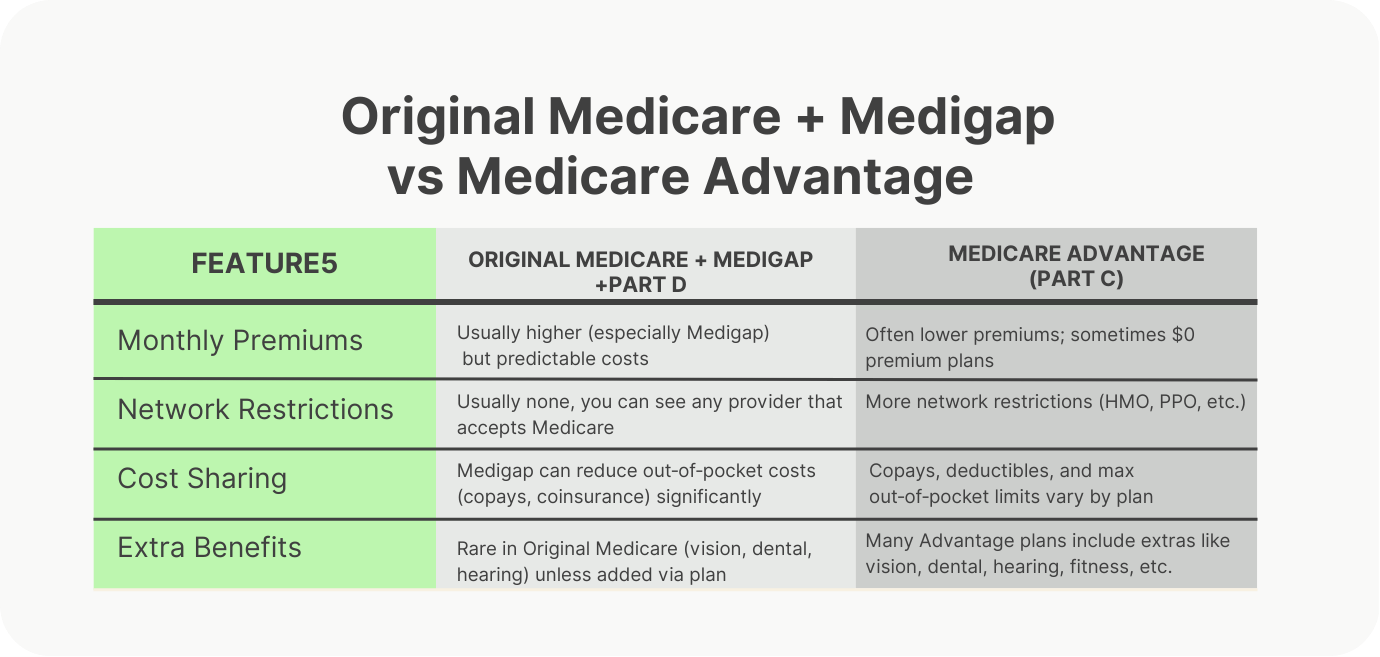

5. What’s the Difference Between Medicare Advantage vs Original Medicare + Medigap?

Medicare Advantage vs Original Medicare + Medigap comparison chart

6. How Do I Sign Up & What Forms Do I Need?

If you’re enrolling in Part A and/or Part B around age 65, Social Security handles your enrollment.

If you qualify for a Special Enrollment Period, or if you’re applying outside the initial window, you may need some forms: e.g. CMS‑40B (for Part B), CMS‑L564 (proof of employer coverage), or CMS‑10797/10798 for special situations.

For comparing plans (Medicare Advantage vs Part D vs Medigap) you can use Medicare.gov’s plan finder tools.

7. Where Can I Get Help & Reliable Information?

These are your best sources:

Medicare.gov— the official U.S. government site. Especially the “Medicare Costs” section and “Get help paying costs.”

CMS.gov — for detailed policy, statistics, official announcements. For example, see the 2025 Medicare Parts A & B Premiums and Deductibles fact sheets.

State Health Insurance Assistance Programs (SHIPs) — free counseling in your state.

Licensed agents or brokers who represent multiple carriers (not just one insurance company).

Final Thoughts

Medicare doesn’t have to be overwhelming but it does require attention.

Here are the key takeaways:

Enroll on time to avoid penalties and gaps in coverage.

Estimate your real costs: premiums + deductibles + what you’ll pay for prescriptions.

Compare Original Medicare + Medigap vs Medicare Advantage using your ZIP code, current doctors, and prescriptions.

Use official resources (Medicare.gov, CMS factsheets) so you’re getting accurate, up‑to‑date info.

Want help reviewing your options? Book a call with our licensed independent Medicare advisors. Our service is free, and afterward, you also get access to our service team for the life of your policy.

.png)

.png)

.png)

.png)

.png)